Trip Insurance Plans Your Travel Safety Net

Trip insurance plans are your best friend when venturing into the unknown. They offer a safety net for unexpected events, transforming potential travel nightmares into manageable bumps in the road. Whether you’re a seasoned globetrotter or a first-time adventurer, understanding the different types of coverage and how to choose the right plan is crucial for a worry-free trip. This guide will walk you through everything you need to know, from choosing the right plan to filing a claim.

We’ll explore various plan types, factors influencing costs, the claims process, and essential benefits beyond medical emergencies. We’ll also help you identify reputable providers and understand policy limitations. By the end, you’ll be equipped to make informed decisions and protect your investment in your next adventure.

Types of Trip Insurance Plans

Choosing the right trip insurance plan can feel overwhelming, but understanding the different types available makes the process much simpler. This section breaks down the key differences between common plans, helping you select the best fit for your travel needs and budget. Remember, the specifics of coverage can vary between providers, so always read the fine print carefully.

Trip insurance plans aren’t one-size-fits-all. They range from basic coverage for essential needs to comprehensive plans that cover a wide array of potential issues. Understanding the differences is crucial to making an informed decision.

Trip Insurance Plan Comparison

The following table compares four common types of trip insurance plans. Consider your trip’s length, destination, and your personal risk tolerance when making your selection.

| Plan Type | Coverage | Cost Factors | Best Use Cases |

|---|---|---|---|

| Basic | Typically covers trip cancellation due to specific, limited reasons (e.g., severe illness or injury), and sometimes medical emergencies. Often excludes baggage loss or flight delays. | Lower premiums; coverage limits are often low. | Short trips, low-risk destinations, travelers with minimal concerns about unforeseen events. |

| Comprehensive | Covers a wide range of events, including trip cancellation/interruption for various reasons (illness, weather, job loss, etc.), medical emergencies, lost luggage, flight delays, and potentially other unforeseen circumstances. | Higher premiums; broader coverage and higher limits. | Long trips, high-risk destinations, travelers concerned about various potential issues, or those traveling with significant financial investments in their trip. |

| Single-Trip | Covers a single, specific trip with defined start and end dates. | Cost depends on the length and destination of the trip, and the level of coverage selected (basic or comprehensive). | Most travelers for one-time trips of any length or destination. |

| Annual Multi-Trip | Covers multiple trips within a year, typically with a specified maximum trip length per trip. | Premium is paid once annually; cost-effective for frequent travelers. | Frequent travelers, those taking multiple short trips throughout the year. |

Coverage Details by Plan Type

The level of coverage for medical emergencies, trip cancellations, lost luggage, and flight delays varies significantly between plan types and providers. Let’s examine these key areas:

Medical Emergencies: Basic plans may offer limited medical expense coverage, while comprehensive plans usually provide more extensive coverage, including medical evacuation if necessary. Always check the policy’s maximum coverage amount.

Trip Cancellations: Cancellation coverage is a key feature. Basic plans often restrict coverage to specific reasons, whereas comprehensive plans cover a wider range of circumstances, such as severe weather, job loss, or family emergencies. Specific reasons for cancellation are usually detailed in the policy document.

Lost Luggage: Comprehensive plans typically offer coverage for lost, stolen, or damaged luggage. Basic plans often exclude this coverage entirely or offer very limited reimbursement.

Flight Delays: Coverage for flight delays is less common, even in comprehensive plans. When included, it usually covers expenses incurred due to significant delays, such as overnight accommodation or meals.

Choosing the Right Trip Insurance Plan: A Decision Flowchart

The following flowchart helps visualize the decision-making process. It’s a simplified representation, and individual circumstances may require more detailed consideration.

(Note: A visual flowchart would be included here. It would start with a question like “What is the length of your trip?”, branching to “Short Trip” or “Long Trip”. Further branches would ask about destination risk, budget, and desired coverage level, ultimately leading to a recommendation of the appropriate plan type.) The flowchart would visually represent the decision-making process, starting with the trip length and progressively narrowing down the options based on risk assessment, budget, and desired coverage.

Factors Affecting Trip Insurance Costs

Getting trip insurance is a smart move, but the price can vary wildly. Understanding what drives those costs helps you shop smarter and get the best coverage for your buck. Several key factors influence how much you’ll pay for your policy.

Several factors significantly impact the final cost of your trip insurance. These factors interact, meaning a higher value in one area might increase the overall cost even if other factors are low. For example, a long trip to a high-risk destination for an older traveler will naturally command a higher premium than a short trip domestically for a young, healthy individual.

Age and Pre-existing Medical Conditions

Your age plays a significant role in determining your trip insurance premium. Older travelers generally face higher premiums because the likelihood of needing medical care increases with age. Similarly, pre-existing medical conditions can dramatically increase your costs. Insurers assess the potential risk associated with your health history, and those with pre-existing conditions that might be exacerbated during travel often pay more. For example, someone with a heart condition traveling to a high-altitude location would be considered a higher risk than a healthy individual traveling to the same location. It’s crucial to disclose all relevant medical information accurately to avoid coverage issues.

Trip Length and Destination

The longer your trip, the higher the risk of something going wrong, thus leading to a higher premium. A week-long trip will typically cost less to insure than a month-long adventure. Your destination also significantly impacts the cost. Travel to regions with unstable political situations, limited medical facilities, or a high incidence of certain illnesses will usually result in higher premiums. For instance, a trip to a remote trekking location in Nepal will cost more to insure than a trip to a major European city. The level of risk associated with the destination is a key factor in premium calculation.

High-Risk Activities

Engaging in high-risk activities while traveling significantly increases your insurance premium. These activities expose you to a greater chance of injury or illness, leading to higher claims for the insurer. Examples of high-risk activities include extreme sports like skydiving, mountaineering, scuba diving (beyond recreational depths), and motorcycling. Participating in such activities may require purchasing specialized adventure travel insurance or result in significant surcharges to your standard policy. For instance, adding coverage for scuba diving to a standard travel insurance policy will increase the cost considerably compared to a policy that only covers standard tourist activities.

Strategies for Minimizing Trip Insurance Costs

It’s possible to reduce trip insurance costs without sacrificing crucial coverage. Here are some effective strategies:

- Travel during the off-season: Premiums are often lower during less popular travel times.

- Book your trip insurance early: Waiting until the last minute may limit your options and increase costs.

- Compare quotes from multiple insurers: Prices can vary significantly between providers.

- Consider a comprehensive policy with a higher deductible: A higher deductible lowers your premium, but you’ll pay more out-of-pocket if you need to file a claim.

- Avoid unnecessary add-ons: Opt for coverage that meets your specific needs, avoiding extras you may not require.

- Travel with a reputable tour operator: Their existing insurance policies may cover some aspects of your trip.

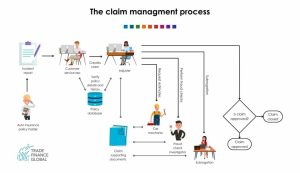

Claim Process and Procedures

Filing a claim with your trip insurance provider is a crucial step if something unexpected happens during your travels. Understanding the process beforehand can significantly reduce stress and improve your chances of a successful claim. This section details the steps involved, common claim scenarios, and how to appeal a denied claim.

The claim process typically begins by notifying your insurance provider as soon as reasonably possible after the covered event occurs. This notification is usually done via phone or online through their website. Following notification, you’ll need to gather all necessary documentation and submit a formal claim. The specific documentation required will depend on the nature of your claim but generally includes proof of purchase for your insurance policy, proof of the covered event (e.g., medical bills, flight cancellation confirmation), and any other relevant supporting documents. Processing times vary depending on the insurer and the complexity of the claim, but you can usually expect a response within a few weeks.

Claim Filing Steps

The steps involved in filing a trip insurance claim generally follow this sequence:

- Notify your insurer: Contact your insurance provider immediately after the covered event. Note the claim reference number provided.

- Gather necessary documentation: Collect all relevant documents supporting your claim (see examples below).

- Submit your claim: Submit your completed claim form and supporting documentation via mail, fax, or online portal, as instructed by your insurer.

- Track your claim: Monitor the progress of your claim through your insurer’s online portal or by contacting customer service.

- Receive your payment (if approved): Once your claim is processed and approved, you will receive payment according to the terms of your policy.

Appealing a Denied Claim

If your claim is denied, you have the right to appeal the decision. The appeal process usually involves submitting additional documentation or providing further explanation to support your claim. Carefully review the denial letter to understand the reasons for the denial and gather any evidence that contradicts their findings. The appeal process and required documentation will be Artikeld in your policy documents or on your insurer’s website. Contacting your insurer directly to discuss the denial and explore the appeal options is highly recommended.

Common Claim Scenarios and Required Documentation

Here are some common claim scenarios and the documentation you’ll typically need to support them:

| Claim Scenario | Required Documentation |

|---|---|

| Trip Cancellation due to Illness | Doctor’s note confirming illness, flight cancellation confirmation, original trip itinerary, and proof of non-refundable expenses. |

| Medical Emergency | Medical bills, doctor’s reports, hospital discharge summary, proof of payment (if applicable), police report (if applicable). |

| Lost Luggage | Airline’s lost luggage report, photos of the lost luggage, receipts for purchased replacement items (if applicable), proof of baggage claim tag. |

| Flight Delay | Airline’s delay confirmation, proof of additional expenses incurred due to the delay (e.g., hotel receipts, meal receipts), and original trip itinerary. |

Benefits Beyond Medical Emergencies

Trip insurance isn’t just about covering medical emergencies; many plans offer valuable benefits that protect your trip investment and peace of mind, even if you stay perfectly healthy. These non-medical benefits can significantly enhance your travel experience and provide crucial support during unexpected situations. Let’s explore some of the most common and useful ones.

Trip insurance plans frequently include a range of non-medical benefits designed to mitigate the financial and logistical burdens associated with unforeseen travel disruptions. Understanding these benefits can help you choose a plan that best suits your needs and travel style, ensuring you’re adequately protected against a variety of potential problems.

Trip Interruption Coverage

Trip interruption coverage reimburses you for prepaid, non-refundable trip expenses if your trip is cut short due to unforeseen circumstances. This could include things like a family emergency, severe weather impacting your destination, or even a sudden illness of a travel companion (provided it’s covered under the policy terms). For example, imagine a sudden family emergency requiring you to return home early from a two-week European vacation. Trip interruption coverage could help reimburse you for the cost of your unused flights, hotel bookings, and pre-paid tours.

Baggage Loss or Delay Coverage

Losing your luggage or experiencing a significant delay in its arrival can be incredibly stressful and inconvenient. Baggage loss or delay coverage helps alleviate this burden by reimbursing you for the cost of essential items you need to purchase while waiting for your luggage to arrive. This can include clothing, toiletries, and other necessities. For instance, if your checked bag is lost on a flight to a tropical destination, this coverage can help you buy new swimwear, sunscreen, and other essentials until your bag is located.

Emergency Assistance Services, Trip insurance plans

Many trip insurance plans include access to 24/7 emergency assistance services. This can be invaluable in a crisis. These services can provide assistance assistocating doctors, arranging medical evacuations, replacing lost or stolen documents, providing emergency funds transfers, and even offering travel advice and support. Consider this scenario: you’re stranded in a foreign country with a lost passport. Emergency assistance services can help you contact your embassy, get an emergency passport, and book a flight home.

- Example 1: A volcanic eruption forces the closure of an airport, delaying your return flight and necessitating additional hotel stays. Trip interruption coverage can reimburse you for these unplanned expenses.

- Example 2: Your flight is cancelled due to a canceled and you miss a pre-booked cruise. Trip interruption coverage can help cover the cost of the missed cruise.

- Example 3: Your luggage is lost on a connecting flight, leaving you without essential medications. Baggage delay coverage can help you replace those medications quickly.

- Example 4: You fall ill while traveling and require immediate medical attention. Emergency assistance services can help you find a local doctor and arrange for transportation to the hospital.

Choosing a Reputable Provider: Trip Insurance Plans

Selecting the right trip insurance provider is crucial for peace of mind during your travels. A reputable provider will offer comprehensive coverage, efficient claims processing, and excellent customer service, ensuring a smooth experience should unexpected events occur. Choosing poorly can leave you financially vulnerable and dealing with unnecessary stress during an already challenging situation.

Choosing a provider involves more than just comparing prices; you need to carefully evaluate their stability and track record.

Provider Financial Stability and Customer Reviews

Checking a provider’s financial strength is paramount. A financially unstable company might not be able to pay out claims when you need them most. Look for providers with high ratings from independent financial rating agencies. These agencies assess a company’s ability to meet its financial obligations. Simultaneously, thoroughly researching customer reviews on independent platforms like Trustpilot or Yelp provides valuable insights into the provider’s responsiveness, claims processing speed, and overall customer satisfaction. Negative reviews often highlight potential red flags, such as slow response times or difficulties in getting claims approved. Pay attention to the volume and consistency of reviews; a few isolated negative reviews are less concerning than a pattern of negative experiences.

Comparison of Trip Insurance Providers

The following table compares three hypothetical providers – it’s crucial to conduct your own research based on your specific needs and destination. Remember that features and ratings can change, so always check the latest information on the provider’s website and independent review sites before making a decision.

| Provider Name | Key Features | Customer Reviews (Hypothetical Average Score) | Financial Stability Rating (Hypothetical) |

|---|---|---|---|

| TravelSafe Insurance | Comprehensive medical coverage, trip cancellation/interruption, baggage loss, 24/7 assistance | 4.5 out of 5 stars | A+ |

| WorldWide Travelers | Worldwideoverage, trip cancellation, emergency medical evacuation, rental car insurance | 4.0 out of 5 stars | A- |

| Global Journey Protection | Basic medical coverage, trip cancellation, limited baggage coverage | 3.5 out of 5 stars | B+ |

Understanding Policy Exclusions and Limitations

Trip insurance, while offering valuable protection, isn’t a blanket guarantee for every eventuality. Understanding the exclusions and limitations within your policy is crucial to avoid disappointment and financial hardship if something goes wrong. Knowing what isn’t covered helps you make informed decisions and potentially supplement your coverage where necessary.

Trip insurance policies typically exclude coverage for certain pre-existing medical conditions, unless you purchase specific add-ons. They also frequently have limitations on the amount of coverage provided for specific events or may exclude certain activities altogether. These exclusions and limitations are clearly defined in the policy documents, and reviewing them carefully before your trip is essential.

Common Exclusions and Limitations

Policy exclusions vary depending on the insurer and the specific plan you choose. However, some common exclusions and limitations include pre-existing medical conditions (unless specifically covered by an add-on), activities considered high-risk (like extreme sports), acts of war or terrorism, and losses resulting from your negligence. Limitations often apply to the maximum amount of coverage for medical expenses, trip cancellations, and baggage loss. Understanding these limitations is key to assessing whether the policy adequately protects your investment.

Implications of Exclusions and Limitations on Coverage

The implications of these exclusions and limitations can be significant. If an event occurs that falls under an exclusion, you won’t receive any compensation from your insurer. Similarly, if your expenses exceed the policy’s coverage limits, you’ll be responsible for the difference. This could lead to substantial out-of-pocket costs, potentially negating the benefits of having insurance in the first place. Therefore, a thorough understanding of these aspects is vital before purchasing a policy.

Examples of Scenarios Where Coverage Might Be Denied

It’s important to understand that the specific circumstances surrounding each claim will be evaluated by the insurance company. However, here are a few examples of scenarios where a claim might be denied due to policy exclusions:

- Pre-existing condition: You purchased a standard trip insurance policy without adding coverage for pre-existing conditions. You experience a flare-up of a chronic condition during your trip, requiring hospitalization. Your claim for medical expenses may be denied because of the pre-existing condition exclusion.

- High-risk activity: You participate in skydiving, a high-risk activity not covered by your policy, and suffer an injury. Your claim for medical expenses related to the injury will likely be denied.

- Negligence: You leave your luggage unattended in a public place and it’s stolen. Your claim for lost baggage may be denied or partially denied if the insurance company determines your negligence contributed to the loss.

- Acts of terrorism: You are traveling in a region experiencing a terrorist attack and your trip is disrupted. Depending on the specific policy wording, coverage for trip interruption may be excluded or limited in situations involving terrorism.

- Failure to comply with policy terms: You fail to report a lost passport within the timeframe specified in your policy. Your claim for expenses related to obtaining a replacement passport might be denied.

Trip Insurance and Pre-Existing Conditions

Pre-existing medical conditions can significantly impact your trip insurance coverage. Understanding how these conditions are handled is crucial before purchasing a policy, as it can prevent unexpected financial burdens during your trip. This section clarifies the relationship between pre-existing conditions and trip insurance.

Pre-existing medical conditions refer to any health issues you had before purchasing your trip insurance policy. This includes both diagnosed and undiagnosed conditions, even if you haven’t sought treatment for them recently. The impact of pre-existing conditions on your coverage varies greatly depending on the specific policy and the insurer.

Coverage for Pre-Existing Conditions

Many trip insurance policies offer limited or no coverage for medical expenses directly related to pre-existing conditions. However, some policies offer options for purchasing supplemental coverage to address pre-existing conditions. This supplemental coverage usually involves a waiting period (typically ranging from 15 to 90 days) after the policy’s effective date. If you become ill or injured due to a pre-existing condition after the waiting period, the policy may cover related medical expenses, though often with limitations on the amount covered. The exact terms and conditions will vary from policy to policy, and it’s crucial to review the policy wording carefully. For example, a policy might cover 50% of expenses related to a pre-existing condition after a 60-day waiting period, up to a maximum payout of $50,000. Another policy might not cover pre-existing conditions at all unless a specific rider is purchased.

Disclosing Pre-Existing Conditions

Accurate disclosure of pre-existing conditions is paramount when applying for trip insurance. Failing to disclose a relevant medical condition could lead to a denial of your claim if you need to use the policy due to that condition. Insurers rely on the information you provide to assess risk and determine appropriate coverage. Omitting information, even unintentionally, could result in your claim being rejected, leaving you responsible for all medical expenses. For instance, if you have a history of heart problems and fail to disclose this when purchasing trip insurance, a subsequent heart-related incident during your trip might not be covered. Be thorough and honest in your application; if you’re unsure about something, contact the insurer directly to clarify.

Final Review

Planning a trip is exciting, but unexpected events can quickly derail your vacation. Investing in a comprehensive trip insurance plan is a smart move that offers peace of mind. By understanding the various coverage options, factors affecting costs, and the claims process, you can ensure you’re adequately protected. Remember to compare providers, read reviews, and choose a plan that aligns with your specific needs and travel style. Don’t let unforeseen circumstances ruin your dream getaway – protect your investment and travel with confidence!