Best Travel Insurance Options Find Your Perfect Fit

Best travel insurance options aren’t one-size-fits-all. Choosing the right policy can feel overwhelming, but understanding the different types – from single-trip to annual multi-trip coverage, backpacker plans to luxury options – is key. This guide breaks down the essentials, helping you compare coverage, features, and costs to find the perfect fit for your next adventure.

We’ll explore crucial coverage features like medical emergencies, trip cancellations, and lost luggage, explaining their importance and potential financial impact. We’ll also delve into factors influencing cost, such as destination, trip length, and pre-existing conditions, offering tips to find affordable yet comprehensive insurance. Finally, we’ll guide you through the process of choosing a policy, filing a claim, and understanding common exclusions.

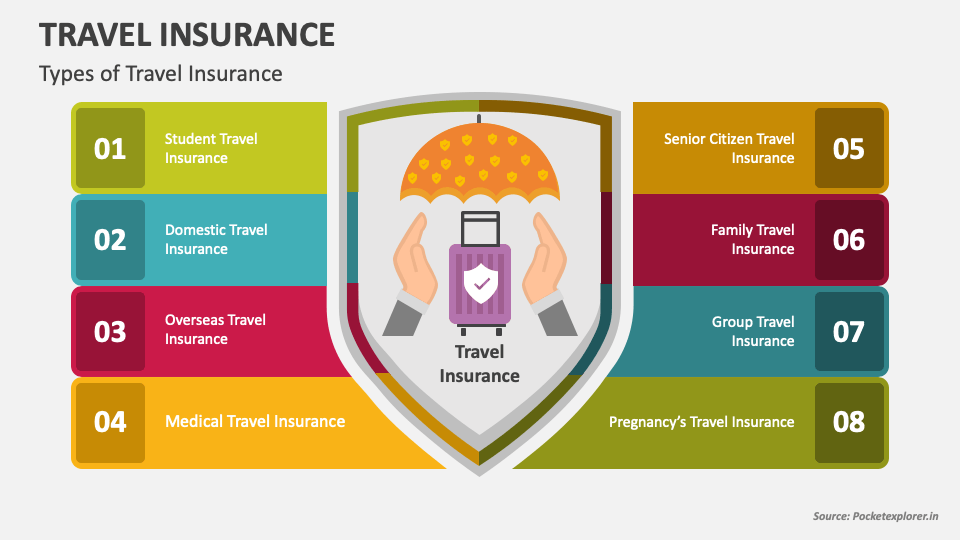

Types of Travel Insurance

Choosing the right travel insurance can feel overwhelming, but understanding the different types available simplifies the process. This section will break down the key categories, highlighting their coverage and price points to help you find the perfect fit for your travel plans. Remember that specific benefits and limitations vary by provider, so always check the policy details carefully.

Single Trip Travel Insurance

Single-trip insurance covers you for a specific journey with pre-defined start and end dates. This is ideal for vacations, business trips, or other short-term travel. Coverage typically includes medical emergencies, trip cancellations, lost luggage, and other unforeseen events during your trip’s duration. However, it won’t protect you if you travel again before purchasing a new policy. The cost is generally calculated based on the length and destination of your trip, with longer trips and more risky destinations commanding higher premiums. For example, a week-long trip to Europe might cost significantly less than a month-long backpacking adventure in South America.

Annual Multi-Trip Travel Insurance

Annual multi-trip insurance is designed for frequent travelers. It provides coverage for multiple trips within a year, typically up to a certain number of days per trip and a maximum overall trip duration. This option offers significant value if you travel several times a year, as it’s often cheaper than buying separate single-trip policies for each journey. Coverage is similar to single-trip policies but extends over the entire policy year. For instance, someone who takes several weekend getaways and a two-week vacation annually would likely find this option more cost-effective.

Backpacker Travel Insurance

Backpacker insurance caters to the needs of long-term travelers, often those engaging in adventurous activities. It typically includes extended coverage periods, broader activity coverage (including things like hiking and trekking), and potentially higher medical expense limits. This is crucial for travelers who plan to be away for months or even years, potentially in remote locations with limited access to medical care. These policies often have higher premiums to reflect the increased risk. A backpacking trip across Southeast Asia, for example, would require a policy tailored to this style of travel, providing coverage for extended durations and a wider range of activities.

Luxury Travel Insurance

Luxury travel insurance is designed for high-net-worth individuals and those traveling with expensive items. It offers higher coverage limits for medical expenses, lost or stolen belongings, and trip cancellations. It may also include additional benefits such as concierge services, 24/7 emergency assistance, and coverage for specific high-value items like jewelry or electronics. The cost reflects the enhanced benefits and higher coverage amounts. Think of a policy that covers a lost diamond necklace or a canceled first-class flight with a significant cost difference.

Cruise Travel Insurance

Specifically designed for cruise vacations, this type of insurance covers trip cancellations, medical emergencies, and other unforeseen events related to the cruise itself. It often includes coverage for things like missed port calls due to ship delays or medical evacuations from a cruise ship. The coverage is typically tailored to the unique aspects of cruise travel, like the specific activities offered on board and potential disruptions to the itinerary. A policy like this could cover medical expenses incurred on a ship, or if a passenger had to miss a port visit due to an unexpected medical event.

| Insurance Type | Typical Coverage | Activity Coverage | Price Range (USD per Trip/Year) |

|---|---|---|---|

| Single Trip | Medical, Trip Cancellation, Lost Luggage | Generally limited to standard activities | $50 – $300+ |

| Annual Multi-Trip | Medical, Trip Cancellation, Lost Luggage | Generally limited to standard activities | $150 – $1000+ |

| Backpacker | Extensive medical, Trip Cancellation, Lost Luggage, Adventure Activities | Often includes hiking, trekking, and other adventure sports | $300 – $1000+ per year |

| Luxury | High limits for medical, trip cancellation, lost/stolen items, concierge services | Broad coverage, often including high-risk activities | $500 – $5000+ per trip |

| Cruise | Medical, Trip Cancellation, Missed Port Calls, Evacuation | Generally covers cruise-related activities | $50 – $200+ |

Key Coverage Features

Choosing the right travel insurance means understanding what’s covered. This isn’t just about peace of mind; it’s about protecting yourself from potentially devastating financial losses. Let’s break down some essential coverage features.

Travel insurance isn’t a one-size-fits-all product. The specific coverage offered will vary between providers and policy types, so always carefully review the policy wording before purchasing. Understanding the potential costs associated with unforeseen events is crucial in determining the level of coverage you need.

Medical Emergencies

Medical emergencies abroad can be incredibly expensive. A simple trip to the doctor can quickly rack up thousands of dollars in bills, especially in countries with high healthcare costs. Travel insurance often covers emergency medical treatment, including hospitalization, doctor visits, and medical evacuations. The policy will usually specify a maximum payout for medical expenses, so it’s important to choose a policy with a limit that’s appropriate for your trip and health status. For example, a policy with a $100,000 medical expense limit would be significantly more beneficial than one with a $50,000 limit for someone traveling to a remote location with limited medical facilities.

Trip Cancellations

Unexpected events can force you to cancel your trip. A sudden illness, a family emergency, or even severe weather can all lead to significant financial losses if you don’t have trip cancellation coverage. This feature will reimburse you for prepaid, non-refundable expenses such as flights, accommodation, and tours. The specific circumstances that qualify for reimbursement will be detailed in your policy. For example, a sudden serious illness requiring hospitalization would usually be covered, while a simple cold or choosing to stay home due to weather would likely not.

Lost Luggage

Losing your luggage can be incredibly stressful, especially if it contains essential medications, valuable electronics, or important documents. Travel insurance often covers the cost of replacing lost or damaged luggage and its contents. However, there are usually limits on the amount of compensation you can receive, and you may need to provide proof of purchase for expensive items. For example, if you lose a suitcase containing $2,000 worth of electronics and clothing, a policy with a $1,500 limit for baggage loss will only cover part of your losses.

Flight Delays

Flight delays can disrupt your travel plans and cause unexpected expenses. Some travel insurance policies offer coverage for expenses incurred due to significant flight delays, such as accommodation and meals. The length of the delay required to trigger coverage will vary between policies, as will the maximum amount reimbursed. For example, a policy might cover expenses if your flight is delayed by more than 12 hours, up to a maximum of $500.

Unexpected Events Covered by Travel Insurance

It’s important to remember that travel insurance can cover a wider range of events than just the basics. Here are five unexpected situations that could be covered:

- Natural Disaster: If a hurricane forces you to evacuate your hotel or delays your return flight, your insurance might cover accommodation and transportation costs.

- Political Unrest: Should a political uprising or civil unrest make your destination unsafe, your policy may cover evacuation costs and trip interruption expenses.

- Terrorist Attack: In the unfortunate event of a terrorist attack impacting your travel plans, coverage might extend to medical expenses, evacuation, and trip cancellation.

- Lost or Stolen Passport: Losing your passport can severely disrupt your travel plans. Insurance can often help cover the cost of replacing it, including expedited processing fees.

- Unexpected Medical Condition: A sudden illness or injury that occurs during your trip and requires hospitalization or medical evacuation is a prime example of when travel insurance is crucial.

Factors Influencing Cost

Getting travel insurance is a smart move, but the price can vary quite a bit. Understanding what drives the cost helps you find the best coverage for your budget. Several key factors influence how much you’ll pay for your policy.

Several interconnected factors determine the final premium you’ll pay for travel insurance. These factors work together to create a personalized price, so understanding each one is crucial for making informed decisions.

Destination, Best travel insurance options

Your travel destination significantly impacts the cost of your insurance. High-risk destinations, known for political instability, natural disasters, or high rates of crime, will generally command higher premiums. For example, a trip to a remote trekking area in Nepal will likely be more expensive to insure than a trip to Paris, France, due to the increased risk of medical emergencies or evacuations in remote areas. Similarly, travel to countries with less developed healthcare systems typically leads to higher premiums because medical evacuations can be costly and complicated.

Trip Duration

The longer your trip, the higher your premium will be. Insurance companies assess risk over time, so a month-long backpacking adventure will cost more than a weekend getaway. This is because there’s a greater chance of something unforeseen happening during a longer trip, increasing the potential payout for the insurer. For instance, a 10-day trip to Europe might cost $50, while a 30-day trip to the same region might cost closer to $150, reflecting the increased duration and associated risk.

Age

Age is a significant factor because the risk of medical emergencies increases with age. Older travelers are generally considered higher risk and, therefore, pay more for insurance. A 65-year-old traveler will likely pay significantly more than a 25-year-old traveler for the same coverage, reflecting the increased likelihood of requiring medical attention. This is not discriminatory; it’s simply an actuarial assessment of risk based on statistical data.

Pre-existing Medical Conditions

Pre-existing medical conditions can substantially affect the cost of travel insurance, sometimes even making it impossible to obtain coverage without additional riders or exclusions. Conditions requiring ongoing medication or treatment often lead to higher premiums or the need for specialized policies. For example, someone with a heart condition might find their premiums significantly higher than someone without any pre-existing conditions, or they might need to pay extra for specific coverage related to their condition. It’s crucial to disclose all pre-existing conditions accurately when applying for travel insurance. Failure to do so could lead to claims being denied.

Finding Affordable Travel Insurance

Finding affordable travel insurance doesn’t mean compromising on essential coverage. Compare quotes from multiple insurers. Look for policies that offer the coverage you need at a price you can afford. Consider increasing your deductible to lower your premium, but only if you can comfortably afford the higher out-of-pocket expenses in case of a claim. Carefully review policy exclusions and limitations. Purchasing travel insurance well in advance of your trip can sometimes help you secure better rates.

Choosing the Right Policy: Best Travel Insurance Options

Finding the perfect travel insurance policy feels like navigating a maze, but it doesn’t have to be overwhelming. The key is understanding your specific needs and comparing policies accordingly. This section will guide you through the process of selecting the right coverage to ensure a worry-free trip.

Choosing the right travel insurance policy involves careful consideration of your travel style, destination, and planned activities. You need to weigh the level of coverage against your budget and the potential risks associated with your trip. A comprehensive comparison of different policies is crucial to making an informed decision.

Policy Selection Based on Individual Needs and Travel Plans

Begin by honestly assessing your travel plans. Are you a solo backpacker venturing off the beaten path, a family with young children needing extensive medical coverage, or a business traveler needing cancellation protection? Your trip’s length, destination, and activities all influence your insurance needs. For example, a high-risk adventure trip requires more comprehensive coverage than a relaxing beach vacation. Consider factors like the cost of your trip, potential medical expenses at your destination, and the likelihood of trip cancellations or interruptions. The more expensive your trip and the higher the potential risks, the more comprehensive your insurance should be.

Step-by-Step Guide to Comparing Travel Insurance Policies

- Identify Your Needs: List your priorities. Do you need extensive medical coverage, trip cancellation protection, baggage loss coverage, or emergency evacuation assistance? Prioritize these needs based on your trip’s specifics.

- Get Quotes: Obtain quotes from multiple insurers. Use comparison websites or contact insurers directly. Ensure you’re comparing apples to apples – policies with similar coverage levels.

- Compare Policy Details: Carefully review each policy’s terms and conditions, paying close attention to exclusions and limitations. Look for clear explanations of coverage amounts, deductibles, and claim processes.

- Check Customer Reviews: Research the insurer’s reputation. Read online reviews to gauge their responsiveness and efficiency in handling claims.

- Consider the Price: While cost is a factor, don’t prioritize it over adequate coverage. A slightly more expensive policy offering better protection might be worthwhile in the long run.

- Make Your Decision: Once you’ve compared policies, choose the one that best balances your needs, budget, and the insurer’s reputation.

Comparison of Three Hypothetical Travel Insurance Plans

The following table compares three hypothetical travel insurance plans tailored to different traveler profiles:

| Feature | Solo Backpacker (Adventure Plan) | Family with Young Children (Family Plan) | Business Traveler (Executive Plan) |

|---|---|---|---|

| Medical Coverage | $1,000,000 | $500,000 per person | $250,000 |

| Trip Cancellation/Interruption | 100% of prepaid, non-refundable expenses up to $5,000 | 100% of prepaid, non-refundable expenses up to $10,000 | 100% of prepaid, non-refundable expenses up to $15,000 |

| Baggage Loss/Delay | $1,000 | $2,000 per person | $3,000 |

| Emergency Evacuation | Included | Included | Included |

| 24/7 Assistance | Included | Included | Included |

| Approximate Cost (7-day trip) | $100 | $250 | $150 |

Note: These are hypothetical examples and actual costs and coverage may vary significantly depending on the insurer, destination, and trip duration.

Filing a Claim

Filing a travel insurance claim can seem daunting, but understanding the process and gathering the necessary documentation beforehand can significantly ease the process and improve your chances of a successful claim. Remember, prompt action is key. The sooner you report your issue, the smoother the process will likely be.

The general procedure involves reporting the incident to your insurer as soon as reasonably possible, usually within a specified timeframe articulated in your policy documents. This initial report is crucial and should include a concise description of the event, the date and time it occurred, and the location. Following this initial report, you’ll need to submit a formal claim, typically through a designated online portal or by mail, accompanied by all required supporting documentation.

Required Documentation

The specific documents required will vary depending on the nature of your claim and your insurance provider. However, common documents include a copy of your insurance policy, a completed claim form (provided by your insurer), a detailed description of the incident, and supporting evidence such as medical bills, police reports, flight cancellation confirmations, or receipts for lost or stolen items. For medical claims, you’ll typically need detailed medical records from your doctor or hospital, including diagnoses and treatment plans. For lost luggage, you’ll need a police report and documentation from the airline. It is essential to keep meticulous records of all expenses incurred as a result of the covered event.

Navigating the Claims Process

Thoroughly read your policy documents before you travel to understand your coverage and the claims process. This will help you avoid misunderstandings and delays later. Keep all receipts, documentation, and communication with the insurer organized in a single file. Take clear photos or videos of any damage or loss, as visual evidence is often crucial in supporting your claim. Respond promptly to any requests for additional information from your insurer and be patient; processing claims takes time. If you encounter any difficulties, don’t hesitate to contact your insurer’s customer service department. Persistence and clear communication are key.

Sample Claim Letter

While the format may vary depending on your insurer, a well-structured claim letter should include the following:

Your Name and Contact Information

Your Policy Number

Date of Incident

Detailed Description of the Incident: Include all relevant facts, dates, times, and locations. For example: “On July 15, 2024, at approximately 10:00 AM, my luggage was lost during my flight from London Heathrow (LHR) to New York JFK (JFK) on flight BA249. The airline confirmed the loss and issued me a Property Irregularity Report (PIR) with reference number 1234567.”

List of Damages or Losses: Be specific about what was lost or damaged and provide the estimated value of each item. For example: “The lost luggage contained clothing, toiletries, and electronics with a total estimated value of $1500.”

Supporting Documentation: Clearly state that you are including all relevant supporting documentation, such as the PIR, police report (if applicable), receipts, and photos.

Claim Amount: Specify the total amount you are claiming.

Your Signature and Date

Example:

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

Subject: Travel Insurance Claim – Policy Number [Your Policy Number]

Dear [Insurance Company Claim Department],

This letter is to formally submit a claim under my travel insurance policy, number [Your Policy Number], for the loss of my luggage on July 15, 2024. [Continue with a detailed description of the incident, list of damages, supporting documentation, and claim amount as Artikeld above].

Sincerely,

[Your Signature]

[Your Typed Name]

Exclusions and Limitations

Travel insurance, while offering valuable protection, isn’t a blanket guarantee. Policies typically contain exclusions and limitations that define what isn’t covered. Understanding these is crucial to avoid unpleasant surprises if you need to file a claim. Knowing what’s excluded helps you make informed decisions about your coverage and potentially take steps to mitigate your risks.

Understanding the fine print of your travel insurance policy is essential. Many policies exclude coverage for certain events, activities, or pre-existing medical conditions. These exclusions are often clearly stated in the policy documents, but it’s easy to overlook them. Failing to understand these limitations can lead to significant financial burdens if an unforeseen event occurs during your trip.

Pre-existing Medical Conditions

Many travel insurance policies won’t cover medical expenses related to pre-existing conditions. This means any health issues you had before purchasing the policy might not be covered if they flare up during your trip. For example, if you have a history of asthma and experience a severe attack while traveling, the costs of treatment might not be reimbursed if it’s deemed related to your pre-existing condition. Some policies offer options to add coverage for pre-existing conditions, often for an additional premium, but there are usually waiting periods involved. It’s vital to disclose all pre-existing conditions accurately when applying for travel insurance.

Adventure Activities

Travel insurance policies often exclude or limit coverage for injuries or accidents sustained during high-risk activities. This can include things like bungee jumping, skydiving, scuba diving, mountaineering, and other extreme sports. The definition of “adventure activity” varies between insurers, so carefully review your policy’s specific wording. If you plan on participating in such activities, you might need to purchase specialized adventure travel insurance or consider additional coverage riders.

Certain Types of Losses

Standard travel insurance policies typically have limitations on the types of losses they will cover. For instance, losses due to acts of terrorism or war are frequently excluded or subject to specific limitations. Similarly, losses caused by negligence or recklessness on the part of the traveler might not be covered. Policies may also have specific limits on the amount they will pay for lost or stolen baggage, often capped at a certain value per item or trip. Understanding these limitations is crucial for determining the appropriate level of coverage for your needs.

Visual Representation of Common Exclusions and Limitations

Imagine a Venn diagram. The largest circle represents all possible travel mishaps. A smaller circle within it represents what is typically covered by standard travel insurance (medical emergencies, trip cancellations due to unforeseen circumstances, lost luggage). Outside this circle are the exclusions: a section for pre-existing medical conditions, another for adventure activities, and a third for losses due to war, terrorism, or traveler negligence. These excluded areas show the gaps in coverage where you might be responsible for costs yourself. Overlapping areas might represent situations where coverage is partial or subject to specific conditions and limitations (e.g., limited coverage for lost luggage). This visual demonstrates that while travel insurance provides a safety net, it doesn’t cover everything.

Summary

Finding the best travel insurance is about more than just ticking boxes; it’s about peace of mind. By understanding the various types of coverage, factors influencing cost, and the claims process, you can confidently select a policy that aligns with your travel style and budget. Remember to read the fine print, compare options carefully, and prioritize essential coverage to ensure a worry-free journey. Happy travels!